On May 10, 2019, the Trump Administration officially increased the 10 percent Section 301 punitive tariff on $200 billion imports from China to 25 percent. Earlier in the week, through his tweet, President Trump further threatened to impose the punitive tariff on all imports from China, including apparel and other consumer products. The escalating U.S.-China tariff war has attracted new attention to the outlook of China as a sourcing destination for apparel. It is also of particular concern that the punitive tariffs will lead to a price hike in the U.S. market, hurting both fashion retailers and consumers.

By using EDITED, a big-data tool for the fashion industry, this article intends to explore how U.S. apparel retailers are adjusting their sourcing strategy for “Made in China” in response to the tariff war. Particularly, based on a detailed analysis of the real-time pricing, inventory and product assortment information of more than 90,000 fashion retailers and their 300,000,000 apparel items at the stock-keeping-unit (SKU) level, this article offers more insights into what is happening in the U.S. retail market beyond what macro-level trade statistics typically can tell us.

Three findings are of note:

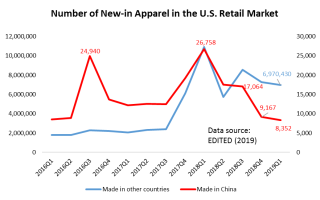

First, U.S. fashion brands and retailers are sourcing less from China, particularly in quantity. Actually, since the Trump Administration launched the Section 301 investigation against China back in August 2017, U.S. apparel retailers had started to include less “Made in China” in their new product offers. Notably, the number of “Made in China” apparel SKUs newly launched to the market had significantly dropped from 26,758 SKUs in the first quarter of 2018 to only 8,352 SKUs in the first quarter of 2019 (Figure above). Over the same period, U.S. apparel retailers’ new product offers that were sourced from other regions of the world stay stable.

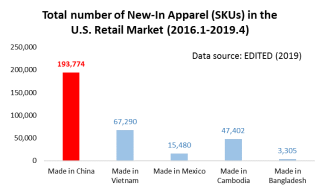

Nevertheless, consistent with the macro-level trade statistics, China remains the single-largest apparel supplier to the U.S. retail market. For example, for those apparel SKUs newly launched to the U.S. retail market between January 2016 and April 2019 (the most recent data available), the total SKUs of “Made in Vietnam” was only one-third of “Made in China,” suggesting China’s unparalleled production and export capacity (i.e., the breadth of products China can make).

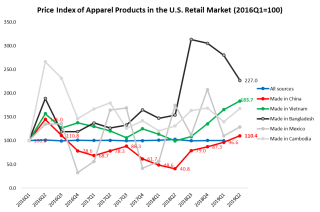

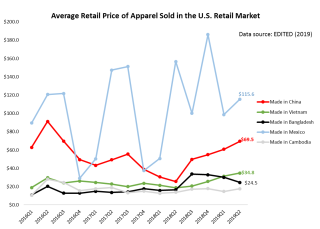

Second, apparel “Made in China” is becoming more expensive in the U.S. retail market, yet remains price-competitive overall. Even though the Trump Administration’s Section 301 action has not targeted apparel products directly, the average retail price for apparel sourced from China in the U.S. market nevertheless has kept rising steadily since the second quarter of 2018. Specifically, the average retail price of clothing “Made in China” has substantially increased from $25.7 per unit in the second quarter of 2018 to $69.5 per unit in April 2019. However, the result also shows that the retail price of “Made in China” apparel was still lower than products sourced from other regions of the world. Notably, apparel “Made in Vietnam” is becoming more expensive in the U.S. retail market too — an indication that as more production is moving from China to Vietnam, apparel producers and exporters in Vietnam are facing growing cost pressures. By comparison, over the same period, the price change of “Made in Cambodia,” and “Made in Bangladesh” stayed relatively stable.

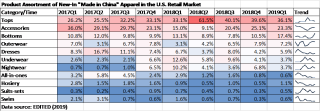

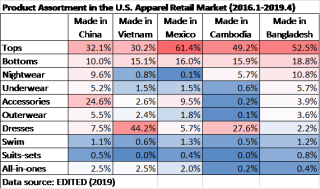

Third, U.S. fashion retailers are shifting what apparel products they source from China. As shown in the following table, U.S. apparel retailers have been sourcing fewer lower value-added basic fashion items (such as tops, and underwear), but more sophisticated and higher value-added apparel categories (such as dresses and outerwear) from China since 2018. This result also reflects China’s continuous efforts in recent years to upgrade its apparel-manufacturing sector and avoid simply competing on price. The shifting product structure could also be a factor that contributed to the rising average retail price of “Made in China” in the U.S. market.

On the other hand, U.S. retailers adopt a very different product assortment strategy for apparel sourced from China versus other regions of the world. In the shadow of the trade war, U.S. retailers may quickly move sourcing orders from China to other suppliers for basic fashion items, such as tops, bottoms, and underwear. However, there seems to be many fewer alternative sourcing destinationsfor more sophisticated product categories, such as accessories and outerwear. Somehow, ironically, moving to source more sophisticated and higher value-added products from China could make U.S. fashion brands and retailers even MORE vulnerable to the tariff war because there are fewer alternative sourcing destinations.

In conclusion, the results suggest that China will remain a critical sourcing destination for U.S. fashion brands and retailers in the near future, regardless of the scenario of the U.S.-China tariff war. Meanwhile, we should expect U.S. fashion companies to continue to adjust their sourcing strategy for apparel “Made in China” in response to the escalation of the tariff war.

Post time: Jun-14-2022